WLMA (Wealth-Lab Moving Average): Indicator Documentation

Syntax

DataSeries WLMA(Bars bars, DataSeries ds, int howManySwings)

Parameter Description

| bars | A Bars object |

| ds | DataSeries to apply WLMA to |

| howManySwings | How many recent swing points to take when computing the indicator |

Description

WLMA (Wealth-Lab Moving Average) is an adaptive, market-driven simple moving average created by Gene Geren. Its lookback period is dynamically changing with market conditions, driven by the

Adaptive Lookback Period indicator.

The WLMA is calculated just like

SMA, but the key difference is that there's no fixed lookback period. WLMA's lookback period is variable-length and is determined by the Adaptive Lookback value obtained using the specified

howManySwings parameter.

Since WLMA heavily depends on Adaptive Lookback, it's advised to review the indicator's

online documentation to understand its construction and interpretation guidelines.

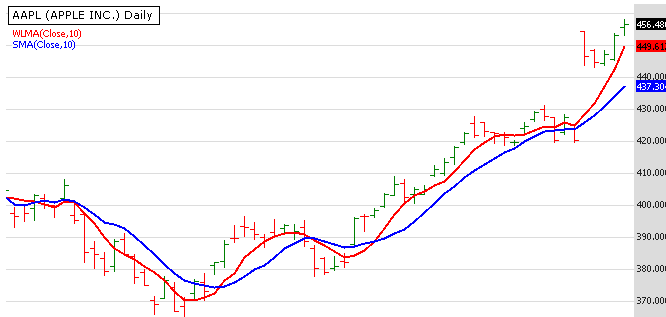

Example

See how more responsive is WLMA (10 last swings) when compared to a short-term 10-bar SMA:

WLMA vs. SMA |