Traders' Tip text

Wealth-Lab owes to C# for the power of extensibility and ability to express trading rules of any complexity. However, its strong point is also that no programming may be required to "wire-frame" a trading system idea.

The Strategy Builder lets us throw building blocks known as Rules onto a "drawing board", group them together or divide them into separate chunks:

- Add a pair of few entry Buy/Sell rules (or Short/Cover if you prefer)

- Drag and drop some "Indicator crosses below (above) a value" and pick "ZScore" from the Community Indicators group (requires Community Indicators library v2019.04 or greater)

- Do the same for "Fast moving average is above (below) Slow moving average" to take trades only if the long term trend is in your favor

- For the exit repeat step #2 with an opposite Z-Score value.

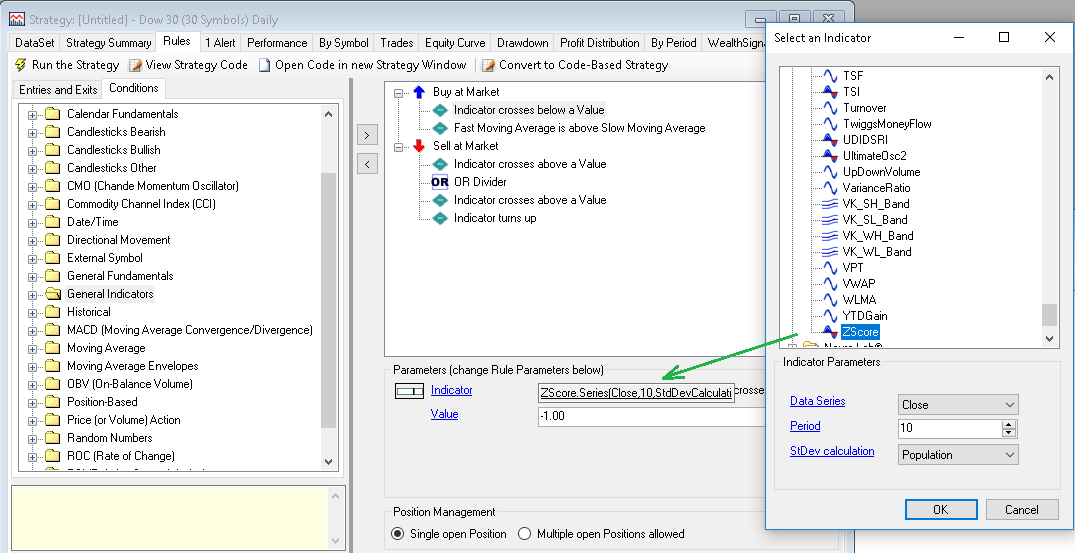

Figure 1. Creating a mean-reversion Strategy in the Rule Wizard.

Figure 1. Creating a mean-reversion Strategy in the Rule Wizard.

There's one more exit rule in author's Python code which liquidates positions if

Z-Score flips from positive to negative or vice versa without going through the neutral zone. As shown on Figure 1, implementing it is a matter of dropping an OR divider with a couple of extra conditions below it.

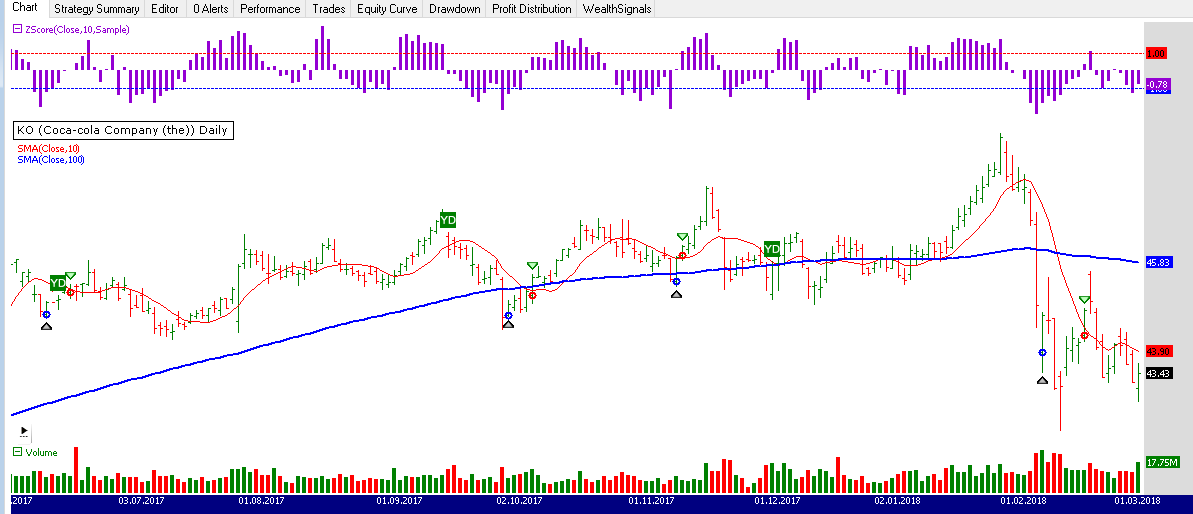

If everything's done right your trading system will generate trades similar to those on Figure 2. Those of you who prefer C# to take complete control will find a sample Strategy code below.

Figure 2. Characteristic trades on a Daily chart of Coca Cola (data provided by Yahoo)

Bottom line:

Figure 2. Characteristic trades on a Daily chart of Coca Cola (data provided by Yahoo)

Bottom line: the advantage of Wealth-Lab over software packages that require coding is that we can come up with a mean reversion system like the one presented by Anthony Garner in a minute of our time.

WealthScript Code (C#)

using System;

using System.Collections.Generic;

using System.Text;

using System.Drawing;

using WealthLab;

using WealthLab.Indicators;

using Community.Indicators;

namespace WealthLab.Strategies

{

public class MeanReversion : WealthScript

{

private StrategyParameter paramPeriod;

public MeanReversion()

{

paramPeriod = CreateParameter("Period", 10, 5, 30, 5);

}

protected override void Execute()

{

int period = paramPeriod.ValueInt;

int lmaPeriod = period * 10;

SMA sma = SMA.Series( Close, period );

SMA lma = SMA.Series( Close, lmaPeriod );

DataSeries zscore = ZScore.Series( Close, period, StdDevCalculation.Sample );

PlotSeries( PricePane, sma, Color.Red, LineStyle.Solid, 1 );

PlotSeries( PricePane, lma, Color.Blue, LineStyle.Solid, 2 );

ChartPane zPane = CreatePane( 30, true, true );

PlotSeries( zPane, zscore, Color.DarkViolet, LineStyle.Histogram, 3 );

DrawHorzLine( zPane, 1.0, Color.Red, LineStyle.Dashed, 1 );

DrawHorzLine( zPane, -1.0, Color.Blue, LineStyle.Dashed, 1 );

//The trigger is a move up or down by more than one standard deviation from the 10-day average price:

//a z-score of over +1 triggers a sell and a z-score of less than -1 triggers a buy.

for(int bar = GetTradingLoopStartBar(1); bar < Bars.Count; bar++)

{

if (IsLastPositionActive)

{

// exit all positions if zscore flips from positive to negative or vice versa

// without going through the neutral zone

if( (zscore[bar - 1] > 0.5 && zscore[bar] < -0.5) ||

(zscore[bar - 1] < -0.5 && zscore[bar] > 0.5) ||

// Clear positions if the z-score between -.5 and .5

Math.Abs(zscore[bar]) < 0.5 )

SellAtMarket(bar+1, LastPosition);

}

else

{

// Buy long if the z-score is < -2 and the longer term trend is positive

if( zscore[bar] < -2 && sma[bar] > lma[bar])

BuyAtMarket(bar+1);

}

}

}

}

}

Gene Geren (Eugene)

Wealth-Lab team